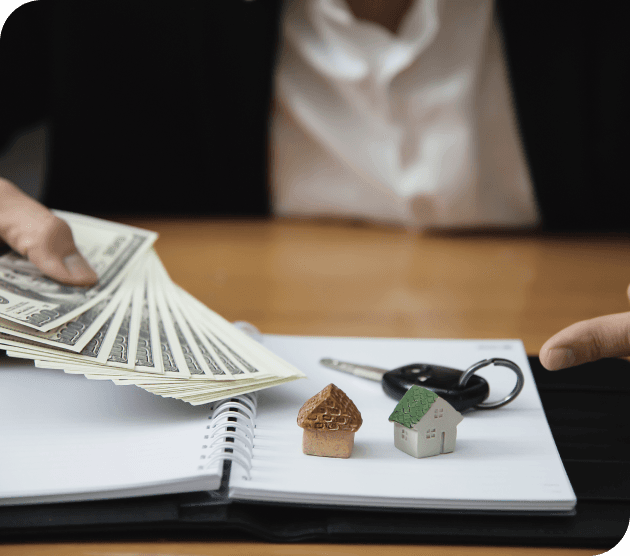

Multifamily Bridge Loans

Delivering customized small balance bridge and permanent loan solutions for Multifamily Real Estate.

Multifamily Bridge Loans

Contact us today for a personalized quote or call us at (866) 575-5070 if you have any questions.

A Note From Don Pelgrim

In the first half of 2026, approximately 76% of multifamily bridge loan requests we received were between $1 million and $10 million, with an average size of $3.4 million. Many of those requests involved acquisitions of multifamily properties with a value-add or stabilization component, indicating the market for turn-around opportunities very remains active.

For multifamily bridge financing, we look closely at the transaction, including, the acquisition price or property basis, current occupancy, capital improvement plan, requested leverage, borrower experience, projected financials at stabilization, and the path to refinance or sale. A value-add multifamily property can be a strong bridge loan candidate and our job as a direct lender is to understand the attributes of the transaction so we can develop capital approaches that align with the transaction needs and help address execution risk.

If you have questions about financing a multifamily acquisition, refinance, or value-add strategy, email me directly at dpelgrim@wilshirefp.com

What Is a Multifamily Bridge Loan?

✓ Purchase/Acquisition

✓ Renovation

✓ Cash-Out Refinance

✓ Bridge-to-Permanent Financing

Multifamily Bridge Loan Program

| Loan Amount | $500,000 to $10,000,000 |

|---|---|

| Term | Up to 3 Years |

| Rate | Fixed or Variable |

| Purpose | Purchase, Rate and Term Refinance, Cash Out Refinance |

| Lien Position | First or subordinate |

| Location | Nationwide |

Multifamily Bridge Loans - Key Benefits

✓ Certainty of Execution

✓ Easier to Obtain

✓ Close in 30 days or less

✓ Perfect for multifaceted transactions requiring expedited timeframes

When to Use a Multifamily Bridge Loan

✓ Tight Timelines

✓ Unstabilized Property

✓ Value-Add Opportunities

✓ Special Situation Lending

Multifamily Bridge Loans vs. Agency/Bank Multifamily Financing

| Institution | Underwriting Timeframe | Minimum Amounts | Term |

|---|---|---|---|

| Bank/Agency | 120 days avg. | $1 million + | 25 - 35 years |

| Wilshire Finance Partners | 15-45 days avg. | $500,000+ | Up to 3 years |

Small Balance Multifamily Bridge Loans

Founded in 2008, Wilshire Finance Partners is a Direct Lender that funds Small Balance Multifamily Bridge Loans using its own money. Borrowers looking for loans on value-add, transitional properties, acquisition, refinance, cash-out, lease-up, repositioning, and other special situations use Wilshire for flexible solutions, speed and certainty of closing.

With loan sizes ranging from $1,000,000 to $10,000,000 and lending nationwide, Wilshire Finance Partners is balance sheet lender and a top choice for real estate investors.

Frequently Asked Questions

What loan product offerings are available for the purchase or refinance of multifamily properties?

Does Wilshire offer bridge and permanent financing for multifamily properties?

Does Wilshire accept loan requests from mortgage brokers, mortgage bankers and banks?

How quickly can Wilshire close a bridge loan on multifamily properties?

Is Wilshire a direct lender?

What are the advantages of financing a multifamily property with Wilshire?

Proven

Real estate debt funds with discretionary capital to lend.

Professional

Experienced professionals representing various disciplines in real estate, banking and investments.

Performance

The team has funded and managed over $3 billion in commercial real estate loans.